Machine Learning: Foundational Assumptions¶

The In-Distribution Assumption¶

Generally: unseen data is drawn from the same distrubtion as your dataset.

Consequence: We don't assume correlation is causation, but we do assume that observed correlations will hold in unseen data.

Model-Specific Assumptions¶

Specific model classes make additional assumptions. For example, linear regression assumes:

- Columns are linearly independent (i.e., one column can't be directly computed from another

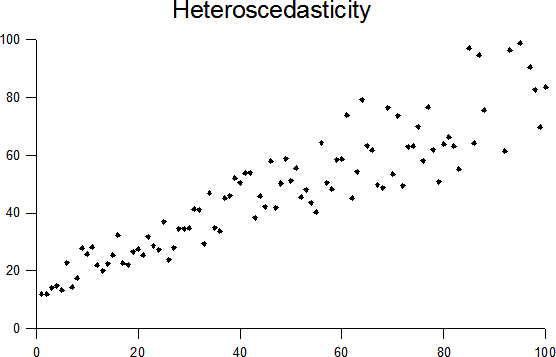

- Data is homoscedastic, i.e., the following won't happen: